A recent report from Key Data reveals a sobering 17% dip in revenue for the U.S. short-term rental market and an 8% decrease in Europe during the summer of 2023. Is it time for short-term rental industry insiders to set off alarm bells? As is often the case with data interpretation, the reality is more nuanced.

While the Key Data report paints a rather bleak picture, another report by AirDNA exudes optimism, boasting record-breaking demand in the United States and a blockbuster summer for Europe during the same period.

But here’s the twist: these seemingly contradictory data sets are not at odds; in fact, they even complement each other in a fascinating way. This clash of perspectives underscores the importance of thorough analysis and comparison when navigating the complex world of data-driven decision-making. For short-term rental owners, hosts, and managers, understanding the nuances and reconciling these perspectives is crucial to making informed choices for your business.

- While on the surface it seems that the Key Data and AirDNA reports contrast, looking deeper at supply growth, Average Daily Rate (ADR) trends, and occupancy rates, the full picture becomes clearer and more cohesive.

- Rising supply has led to lower RevPAR and occupancy rates. But, AirDNA notes a slowing growth rate in supply – just 12.1% YoY in the U.S.

- ADRs are falling, but remember, prices have shot up since 2021. They can’t rise forever and will stabilize soon.

- Lastly, supply outpaced demand in 30 of the top 50 European cities in July but exceptions show local market dynamics heavily at play.

Understanding the Metrics: RevPAR vs. YoY Demand Growth

RevPAR (Revenue Per Available Rental), Key Data’s primary metric, focuses on the financial performance of short-term rentals. It calculates revenue generated per rental unit, taking into account both occupancy rates and average daily rates (ADR). A decline in RevPAR suggests a drop in revenue, which is what Key Data highlighted in its report.

On the other hand, YoY Demand Growth (Year-over-Year Demand Growth), as favored by AirDNA, measures the change in the number of nights booked compared to the same period in the previous year. This metric assesses the demand for short-term rentals. So, when AirDNA talks about record-breaking demand, it’s emphasizing the number of bookings made, which might not directly reflect revenue.

It is also worth noting that the number of nights booked is heavily dependent on how many nights are actually available to book, which can shift with supply changes in a given market.

When viewed in isolation, these metrics can indeed appear contradictory. Key Data’s RevPAR indicates a revenue decline, while AirDNA’s YoY demand growth showcases a surge in bookings. However, the full story emerges when we consider other critical factors, such as supply growth, ADR trends, and occupancy rates, which both reports touch upon.

17% Decline in RevPAR or 2.3%: Which Is It?

The contrasting figures from Key Data and AirDNA’s summer 2023 reports — a 17% and 2.3% decline in Revenue Per Available Rental (RevPAR) respectively — can be confusing. Is one more accurate than the other? If so, which one?

In truth, the accuracy of these reports isn’t in question; rather, the disparities could be explained by the probable difference in methodologies used by each:

1. Reference Period: The timeframes used for comparison contribute significantly to the differences. In its report, AirDNA benchmarks against the previous year, offering a clear year-on-year comparison. It would be useful to determine whether Key Data’s method compares the same period from the prior year or earlier months within the same year, as the choice directly influences the data outcome.

2. August Data Inclusion: Key Data’s report includes August — a peak travel month — which can drastically affect overall summer performance metrics. In contrast, AirDNA’s report stops in July. This variation in reporting periods could lead to different assessments of market conditions.

3. Market Segmentation: Key Data primarily serves traditional vacation rental destinations like mountain and coastal regions, while AirDNA’s report accounts for urban markets as well. It is possible that Key Data’s report skews differently due to the different product mix than that of AirDNA. Given the diverse impacts of the COVID-19 pandemic across these markets, the segmentation could significantly influence data representation.

Revenue Plunge in Times of High Demand: How is This Possible?

The U.S. short-term rental market’s performance in the summer of 2023 is a complex interplay of various factors. The decline in RevPAR and occupancy is not necessarily an indicator of waning demand, as AirDNA’s data underscores historic demand growth.

More Listings Than Ever

The global surge in supply has been instrumental to the decline in RevPAR (Revenue Per Available Rental) and occupancy rates. The addition of more listings has been a priority for all industry players, big and small alike. In fact, Airbnb added more total net active listings in Q2 2023 than any previous quarter, surpassing a noteworthy 7 million total active listings. However, this increase in supply means that bookings are now spread across a larger pool of listings, consequently impacting occupancy rates.

Possible Slowdown in Supply?

AirDNA’s report reveals a slowing supply growth rate of 12.1% YoY in July 2023. This marks a significant slowdown compared to the same period in the previous year, which witnessed a robust growth rate of 24.4% YoY. This could hint at some semblance of balance in the demand-supply dynamics of the industry.

Yet, whether this slowdown will be enough to fully offset the growth in demand remains uncertain.

Moreover, it is not yet clear whether regulatory changes in specific markets, such as New Orleans and New York City, have had any impact on these supply numbers.

Lowering ADRs: Not As Worrying As It May Seem

Key Data’s latest report reveals that ADR experienced an 8.1% year-over-year decrease, dropping from $328 to $302. At face value, this may raise concerns about the profitability of short-term rentals.

However, a deeper understanding of these figures within the framework of ongoing inflation introduces a nuanced perspective. Amid inflationary pressures, a more drastic decline in ADR might be anticipated.

While travelers grapple with the impact of escalating prices due to inflation, the decline in ADR, when adjusted for inflation, is not as severe as one might expect. This suggests that despite nominal price decreases, ADR has demonstrated considerable resilience in real terms.

This resilience of ADR, coupled with travelers’ adaptation to inflation, underscores the fact that while the short-term rental industry is not immune to broader economic trends, it has managed to navigate these challenges with relative success.

Also, let’s not forget that since 2021, vacation rental prices have skyrocketed to dizzying heights. So much so, that Airbnb has had to make it its mission to fight the perception of being expensive. Inflation has been a catalyst, sure, but let’s face it, demand has driven the prices consistently up. Prices can’t keep climbing forever; they’ll have to hit a plateau sooner or later.

Europe and the UK: A Quieter Decline Amidst Recovery

In contrast to the U.S., Europe and the UK witnessed more tempered declines in their performance metrics.

In Europe, a slight increase in Average Daily Rates (ADRs) served as a counterbalance to an 8.2% drop in occupancy, resulting in an 8% decline in Revenue per Available Rental (RevPAR), according to the Key Data report.

In the United Kingdom, we see a somewhat different scenario. There, RevPAR experienced a 6% dip, driven by a 2.4% decrease in occupancy and a 3.6% reduction in ADRs.

While the numbers appear less harsh, they reflect a distinct recovery pace compared to their American counterpart.

While the declines in these regions may seem smaller, they should not be mistaken for better overall market conditions. Instead, they reflect the different stages of recovery that these markets are experiencing.

How the Timeline of Recovery Matters

The U.S. market was already witnessing a surge in early 2021, with demand soaring by +24% compared to 2019. Small city and rural markets were at the forefront, experiencing remarkable growth at +62%.

In contrast, the great European comeback only began to take shape in 2022. The continent’s journey towards recovery was marked by a deliberate pace, as countries cautiously lifted Covid-19 restrictions. This delayed resurgence underscored the diverse timelines of recovery on opposite sides of the Atlantic.

As for the United Kindom, an additional factor contributing to the decline in Average Daily Rates (ADRs) could be the resurgence of smaller city units. As urban demand makes a comeback, smaller city accommodations influencing pricing dynamics.

Think Global, Act Local Remains the Mantra

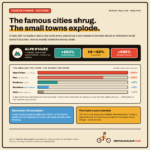

Northern European countries, including Norway (+29.3%), Sweden (+26.3%), and Poland (+21.2%), witnessed remarkable year-over-year demand growth.

However, despite strong demand, certain Scandinavian nations grappled with a supply-demand mismatch.

Year-over-year growth in supply and demand within the top 50 European cities outpaced that of more rural areas and smaller towns and cities as international travel reopened.

Yet, despite this urban resurgence, 30 of the top 50 European cities, experienced year-over-year declines in occupancy in July as supply outpaced demand, except for cities like Vienna and Copenhagen where regulations do not allow for the speedy expansion of supply.

France, on the other hand, saw occupancy levels flourish, in keeping with what we have seen of its recent trajectory as the host of the 2023 Rugby World Cup and the Paris Olympics 2024.

Conclusion:

In the world of short-term rentals, the devil is often in the details, and what matters most is how these trends play out in your specific local market.

Hosts and property managers should remain vigilant, paying close attention to hyperlocal data and accounting for the nuances of their particular market. Factors such as local regulations, seasonal variations, and evolving traveler preferences can significantly impact your strategy.

In our industry, a one-size-fits-all approach seldom applies, making it crucial to tailor your decisions to the specific conditions of your hosting domain. Doing so allows you to chart a course that maximizes your chances of success in the dynamic world of short-term rentals.

Uvika Wahi is the Editor at RSU by PriceLabs, where she leads news coverage and analysis for professional short-term rental managers. She writes on Airbnb, Booking.com, Vrbo, regulations, and industry trends, helping managers make informed business decisions. Uvika also presents at global industry events such as SCALE, VITUR, and Direct Booking Success Summit.