Airbnb has promised Wall Street that in 2026 it will earn more from every booking. Your host fee is not going up, and Airbnb is not dipping into your payout. Both statements are true, and how they fit together is what this article is about.

To be clear: Airbnb is not taking a bigger slice of your booking. It sells more things on top of your booking (insurance, cancellation flexibility, payment options) and keeps the proceeds. Your $1,000 reservation stays a $1,000 reservation for you. For Airbnb, it becomes a $1,000 reservation plus add-ons that never appear on your statement.

You know the 15.5% story. This is the other side.

The move to the mandatory 15.5% host-only fee on October 27, 2025 was debated, modeled, and repriced around; if you followed our markup guidance, your payouts survived the migration. That fight is over. But while managers were watching the host side of the ledger, Airbnb built its growth engine on the other side: insurance and fintech products sold to guests at checkout, or attached to your listings automatically.

Why should you care, if the money comes from guests rather than from you? Because guests travel on a total budget. Every euro or dollar a guest spends on Airbnb’s add-ons is spending power that was available for your nightly rate, your ancillaries, or your direct-booking upsells. Airbnb’s executives now describe these products, on the record, as levers to lift the company’s take rate.

What this article will show you

By the end, you will be able to trace, product by product and dollar by dollar, how Airbnb earns more every time a guest books one of your properties, even though your own fee never moves. We will use Airbnb’s own numbers and its executives’ own words, and we will finish with a worked example on a single $1,000 booking.

One thing before we start: Airbnb is doing what any well-run marketplace with control of its payments would do, and it discusses these products openly with its investors. Our goal is to explain the mechanics, using Airbnb’s own disclosures and quotes. Where we go beyond the facts and add our own interpretation, we will say so.

Key takeaways

- Airbnb’s CFO has named its insurance program, twice, as an official driver of take-rate growth for 2026.

- Guest travel insurance revenue grew about 40% in 2025 and 45% in Q1 2026; analysts size the opportunity at roughly $500 million over three to five years.

- Reserve Now, Pay Later now accounts for about 20% of global booking value, and it raised the platform’s cancellation rate from about 16% to 17%.

- The new extended cancellation option auto-enrolls most listings: guests pay Airbnb for the right to cancel late, and your calendar carries the risk.

- On a single $1,000 booking, these guest-side products can lift Airbnb’s revenue from $155 to over $200 without touching your host fee.

What “take rate” means, in plain terms

Take rate is the share of gross booking value that Airbnb keeps as revenue. A guest pays $1,000 for a stay; if Airbnb’s revenue from that transaction is $140, the take rate is 14%.

Take rate can grow without host fees changing at all. An insurance premium, a flexibility fee, a currency-conversion charge: each one increases Airbnb’s revenue per booking. And since guests travel on a total budget, money captured there is money that was available for your nightly rate.

The CFO says it out loud

CFO Ellie Mertz spelled it out on the Q1 2026 earnings call, answering a Bernstein analyst (full transcript):

“As we called out in the letter, you should see modest upside to our take rate from both the migration to the single fee structure as well as our insurance program.”

And again in the same call’s guidance:

“The upward revision to our revenue outlook reflects meaningful progress across our growth initiatives and improvements to monetization through a simplified fee structure and our insurance program, which are expected to lift our full-year take rate.”

Insurance is named twice, in official guidance, as a take-rate driver. Keep that in mind while we go product by product.

Guest travel insurance: growing 40% a year

Airbnb launched paid guest travel insurance in May 2022, underwritten by Generali and priced as a percentage of the trip cost at checkout. It has nothing to do with the free AirCover protections.

The growth curve, in Airbnb’s own words

- Q4 2022: live in 8 countries; Brian Chesky calls the product “really, really successful.”

- Q3 2025: available in 12 of Airbnb’s largest markets, growing more than 25% year over year.

- Full-year 2025: insurance revenue up about 40%.

- Q1 2026: growth accelerates to roughly 45%.

Analysts have sized the prize. MBI Deep Dives calculates that if insurance expands Airbnb’s take rate by around 50 basis points, that would be worth roughly $500 million in high-margin revenue over three to five years.

Why it costs you, even though guests pay

On your direct-booking site, trip insurance and damage waivers may be your ancillary revenue. On Airbnb, Airbnb sells them and keeps all of it.

The extended cancellation option: Hopper’s product, your calendar

In June 2026, Airbnb rolled out a paid extended cancellation option that lets guests cancel for any reason up to 24 hours before check-in and get a full refund. It launched in 12 countries, including the US, Canada, Ireland, and the Netherlands.

Airbnb’s first fintech product? Not quite

Skift described it as Airbnb’s “first foray into travel fintech.” Actually, Airbnb has been running money-transmitter licenses through Airbnb Payments since its early years, launched in-house installments in 2018, has sold Generali-underwritten travel insurance since 2022, and added Klarna financing in 2023.

What is genuinely new is narrower: this is the first time Airbnb charges guests a fee for absorbing a risk itself, rather than facilitating a payment or brokering someone else’s insurance. First fintech product, no. First monetized risk product, yes.

Three things managers need to know

- You were enrolled automatically. Listings with moderate, limited, firm or strict cancellation policies are in by default; you have to opt out.

- The fee goes to Airbnb. The guest pays at booking for the right to override your cancellation policy.

- You keep the risk. You are still paid per your original policy, but a night released 24 hours before check-in rarely resells. The fee compensates Airbnb. Nothing compensates you for the empty night.

A quick Hopper primer, for readers outside North America

Hopper pioneered this category. If the name doesn’t ring a bell, that is normal for European readers: Hopper is a Montreal-based travel app, huge with Gen Z travelers in the US and Canada but barely present in Europe. It started out predicting flight prices (“book now or wait”), then discovered that the real money was in selling protection against travel uncertainty. At its peak it was valued around $5 billion, and for a while it was the most downloaded travel app in the US ahead of Booking and Expedia. It even entered our industry in 2022 with Hopper Homes, as we analyzed at the time.

What made Hopper different was where its revenue came from. Its fintech products (Price Freeze, Cancel for Any Reason, Instant Travel Refund) generated about half of its revenue by 2022 and drove 40% of its $7.5 billion in 2024 bookings, while traditional OTAs still lived off booking commissions. Not everyone applauded: Expedia terminated its supply deal with Hopper in 2023, accusing it of “exploiting consumer anxiety.”

Where Hopper ended up

A long way from those ambitions. The consumer-app dream of dethroning Airbnb and Booking faded, and Hopper Homes never became a serious challenger. The company pivoted to selling its fintech machinery to other brands through Hopper Technology Solutions, which powered travel programs for Capital One, Tripadvisor and Uber and grew to about two-thirds of the business by mid-2024. Then, in late 2025, Capital One bought the technology and the roughly 150 employees behind Capital One Travel, a deal that closed in April 2026.

Hopper proved that travel fintech works, then sold much of the machine to a bank. Airbnb, which has the audience Hopper never had, is now installing the same machinery inside its own checkout, powered by a third party it declines to name, according to Skift.

Reserve Now, Pay Later: Airbnb gets the growth, you get the cancellations

Reserve Now, Pay Later lets guests book eligible stays with zero dollars down and pay closer to check-in. It launched in the US in summer 2025 and went global in Q1 2026. Guests pay nothing extra for it, so where is the fintech? In what it does to the numbers.

What it does for Airbnb

- Roughly 20% of global gross booking value now comes from RNPL bookings (Chesky, May 2026).

- RNPL and the single service fee added about 200 basis points to nights growth and 300 to GBV growth in Q4 2025; the combined product updates added about 3 points of nights and 4 points of GBV growth in Q1 2026 (Mertz).

- It lengthens lead times and nudges average daily rates upward, since “consumers who don’t need to extend a huge purchase on their credit cards are more likely to choose a slightly nicer listing.”

What it costs you

The cost shows up in cancellations. Mertz’s words on the Q4 2025 call:

“In terms of the aggregate nominal increase in cancellations rate, it’s approximately 1%. So an average of maybe 16% cancellation rate historically going to 17%. It’s obviously higher within the cohort that chooses that product.”

A quarter later, she framed it this way: cancellations are higher, “but across all regions, the net impact is positive to the business.” Positive to Airbnb’s business, averaged across millions of listings. The manager whose peak-season week was blocked by a zero-down reservation that evaporated does not live in a portfolio average.

Your policy choice is the opt-in

One more detail: RNPL only applies to listings with moderate or flexible cancellation policies. Your policy choice now decides whether you participate in this trade-off.

Pay-later credit with Klarna, installments in-house

For guests who want actual installment credit, Airbnb has offered “Pay Over Time” with Klarna since May 2023, first in the US and Canada, then the UK, Australia and much of Europe. Klarna carries the credit risk; Airbnb gets paid up front and takes the conversion lift. Airbnb also runs its own split payments, a product line that goes back to 2018’s “Pay Less Up Front” (adopted by nearly 40% of eligible users at launch), plus local installments that Chesky described in May 2026 as “huge in Brazil.”

The fees you never see

Two more fees deserve a mention, if only because almost nobody talks about them.

The cross-currency fee

Introduced mid-2024, it adds roughly 100 basis points on about 20% of GBV. Airbnb’s own math puts that at around 20 basis points of take rate, and the company cited it in its FY2024 results as a revenue driver alongside travel insurance.

The single service fee, revisited

The October 2025 migration was pitched as price transparency and competitiveness. The fact: Mertz names it, alongside insurance, as a source of take-rate upside in 2026 guidance. Our interpretation: a genuinely neutral restructuring would not lift take rate.

One likely mechanism: the 15.5% applies to the entire booking subtotal, cleaning fees and other mandatory charges included, which the old 3% host fee treated differently. Airbnb is now testing the single fee beyond API hosts.

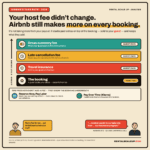

Follow the money on one booking

Let’s make this concrete with an illustrative scenario. Airbnb does not disclose the price of each add-on or its margin on them, so the figures below are our estimates, built from how these products are typically priced. The mechanics, however, come straight from Airbnb’s public materials.

A guest books a week at one of your properties for $1,000 (or €1,000; the mechanics are the same).

Airbnb’s baseline revenue is your host fee: 15.5%, so $155. That is the part you see on your statement, and until recently it was more or less the whole story.

Then come the extras.

At checkout, the guest is offered travel insurance, priced as a percentage of the trip. On a $1,000 booking that typically runs several tens of dollars. Insurers customarily pay their distribution partners a share of each policy sold; Airbnb does not disclose its cut.

In twelve countries, the guest also sees the extended cancellation option. If they buy it, that fee goes to Airbnb, not to you, even though your calendar carries the cancellation risk.

If your guest is French and your property is in Florida, or American and your property is in Portugal, a cross-currency fee of roughly 1% is applied when they pay in their home currency. This detail matters more for European managers, whose international guest mix is structurally higher.

And if the guest used Reserve Now, Pay Later, Airbnb paid nothing for the privilege but statistically gained a longer lead time, a slightly more expensive booking, and a slightly higher chance the reservation dies before check-in.

The same stack, as a table:

| Product | Who pays | Where the money goes | What it means for you |

|---|---|---|---|

| Host service fee (15.5%) | You | Airbnb | The only line you see on your statement |

| Guest travel insurance | Guest | Premium to Generali, distribution share to Airbnb | Competes with the insurance you sell on direct |

| Extended cancellation option | Guest | Fee to Airbnb | You carry the late-cancellation risk; opt-out only |

| Cross-currency fee (~1%) | Guest | Airbnb | Invisible; hits international guest mixes hardest |

| Reserve Now, Pay Later | Nobody (free) | Conversion and ADR lift for Airbnb | More bookings, softer calendar, more cancellations |

| Pay Over Time (Klarna) | Guest (interest/fees to Klarna) | Conversion lift for Airbnb | Klarna’s risk, Airbnb’s growth |

None of these lines appear anywhere in your payout report. Our estimate, and it is only that: on a booking where the guest takes both insurance and the cancellation option, Airbnb’s revenue could move from $155 to somewhere above $200, roughly 30% more earned on your property, without your fee changing by a cent.

You can quarrel with our assumptions; the exact figures vary by trip and market. The direction, however, is not in doubt, because Airbnb itself tells investors these products lift its share of every booking.

This is a roadmap, and Chesky says so

Asked in May 2026 about payment innovations beyond RNPL, Chesky answered:

“We have an entire roadmap around payments and pricing. The payments and pricing roadmap has the opportunity to deliver hundreds of millions of dollars in revenue each year… Reserve Now, Pay Later is uniquely large, but there are dozens of projects that can deliver growth.”

Why Airbnb can do what Booking cannot

Airbnb can do all of this because it is the merchant of record, through its licensed money-transmitter subsidiary Airbnb Payments, Inc. It touches every dollar (over $100 billion in payments a year) and can attach a product to any moment of the transaction.

Compare Booking.com and Vrbo, which partner outward (Affirm powers Vrbo’s pay-later option) and let managers price flexibility themselves through rate plans. That difference matters more than any single fee. In the Booking model, the manager sets a higher rate for a flexible policy and keeps the premium. In the Airbnb model, the platform prices the flexibility and keeps the fee.

The flexibility premium used to be a revenue-management opportunity for the manager. It is becoming Airbnb fintech revenue.

A caveat: the free protection is under regulatory fire

One part of Airbnb’s protection stack generates no revenue: AirCover, including the $3 million Host Damage Protection. Airbnb has always stated in its terms that HDP “isn’t an insurance policy,” and professional managers know it is a discretionary guarantee rather than coverage.

Washington first, Virginia now

Regulators are testing that structure anyway, because insurance law looks at substance, not labels. Washington state fined Airbnb $20,000 in 2023 for acting as an unauthorized insurer and forced it to back HDP with a real surplus-lines policy. The investigation revealed that of 5,525 host claims escalated to Airbnb, about 3,565 were paid, roughly $2.3 million in total.

In June 2026, Virginia’s Bureau of Insurance went further and demanded Airbnb halt HDP in the state until it is licensed or properly underwritten, with a July 31, 2026 deadline to settle or face a December hearing.

Why this belongs in a revenue story

Here we move from facts to our expectation. If regulators force real underwriting costs onto the free product, the rational response is to shrink free protection and grow paid protection. Two facts point that way already: Airbnb tightened HDP claim requirements in April 2026, and it already sells paid host earnings protection with MIC Global in the US.

What a manager should actually do

- Check your enrollment in the extended cancellation option. You were likely enrolled automatically, and the decision to stay in deserves real math, especially for peak weeks.

- Re-run your cancellation-policy numbers under RNPL. Moderate and flexible policies now carry RNPL eligibility along with its cancellation profile, and the platform-wide bump from 16% to 17% understates what happens inside RNPL cohorts.

- Audit what you tell owners about AirCover. “$3M protection from Airbnb” is not insurance and never was; Virginia just made that official. Keep requiring commercial STR coverage on every channel.

- Trust your calendar a little less. A fifth of global GBV is now booked with nothing down. A full calendar is softer than it used to be.

- Build your own version of this on direct. Damage waivers, flexible-cancellation upgrades, trip insurance partnerships: Airbnb has just demonstrated, with 40%-plus annual growth, that guests will pay for peace of mind. On direct bookings, that margin belongs to you.

The 15.5% host fee was the change everyone debated. The guest-side stack is the one nobody voted on: insurance, flexibility fees, deferred payments and FX charges, all earning Airbnb more per booking while your inventory does the work. The numbers above are Airbnb’s own.

Thibault Masson is a leading expert in vacation rental revenue management and dynamic pricing strategies. As Head of Product Marketing at PriceLabs and founder of Rental Scale-Up, Thibault empowers hosts and property managers with actionable insights and data-driven solutions. With over a decade managing luxury rentals in Bali and St. Barths, he is a sought-after industry speaker and prolific content creator, making complex topics simple for global audiences.

Related Articles:

Airbnb May 20 2026 Summer Release: What to Expect, and Why This Update Matters More Than Ever

Airbnb May 20 2026 Summer Release: What to Expect, and Why This Update Matters More Than Ever

Airbnb’s natural language search is already live in the US — five days before the Summer Release

Airbnb’s natural language search is already live in the US — five days before the Summer Release

Airbnb debuts lowest price guarantee, and what looks like a loyalty mechanism – but only for hotels

Airbnb debuts lowest price guarantee, and what looks like a loyalty mechanism – but only for hotels

Airbnb, Booking.com, and Vrbo Are Changing How Listing Visibility Works, and It’s Going to Cost You

Airbnb, Booking.com, and Vrbo Are Changing How Listing Visibility Works, and It’s Going to Cost You